June 2026 Market Snapshot

June 2026 Market Snapshot Staff | July 17, 2026 *The City of Chicago Market Snapshot represents the residential real estate

The Chicago Association of REALTORS®, the “Voice for Real Estate” in Chicago since 1883, represents 16,000+ members from all real estate specialties including commercial sales, development, property management, appraisal, auctions and residential sales.

Learn how we help our 16,000+ members grow their businesses and empower property owners. Membership options are available for licensed real estate professionals and those affiliated with the real estate industry!

Connect with Chicago’s real estate communities and build meaningful relationships! Organized by our own members, we host almost 70+ virtual and in-person events every year.

REALTORS® Real Estate School offers all kinds of real estate licensing and training. Browse self-paced, online training or live classes in our modern, downtown classrooms!

How can we help your business succeed? Your membership includes multiple resource guides on industry topics, tools to increase your knowledge and market statistics to help your serve your communities.

Get the latest in Chicago real estate news. Plus, explore the insight and resources available in the Chicago REALTOR® Magazine digital issues.

Welcome to the Chicago Association of REALTORS® blog and news hub. Explore magazine articles, industry updates and more. You can filter by category or tag based on your interests.

June 2026 Market Snapshot Staff | July 17, 2026 *The City of Chicago Market Snapshot represents the residential real estate

Congratulations To The 2026 REALTOR® Award Winners! Staff | July 15, 2026 Membership Congratulations to the recipients of the 2026

The latest issue of Chicago REALTOR® is now available. Enjoy the content in the format of your choice. You can find the digital PDF flipbook below, with links to blog-format articles. Chicago […]

Chicago REALTORS® Past Presidents Honored During the Illinois REALTORS®’ REALTOR® of the Year Banquet Congratulations to one of our past presidents, Sarah Ware, Ware Realty Group, on being named the […]

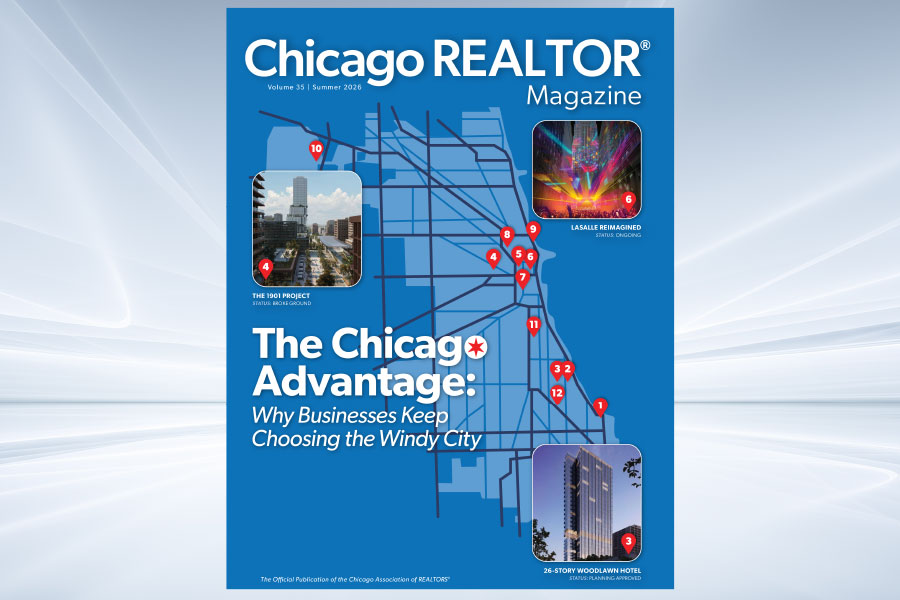

As Chicago REALTORS®, we know what makes this city exceptional: the people, the culture, the lakefront, the iconic skyline and our 77 community areas. Just as important, though often less […]

Chicago REALTOR® Magazine is the only glossy, 4-color publication that covers the entire residential real estate market in Chicagoland.

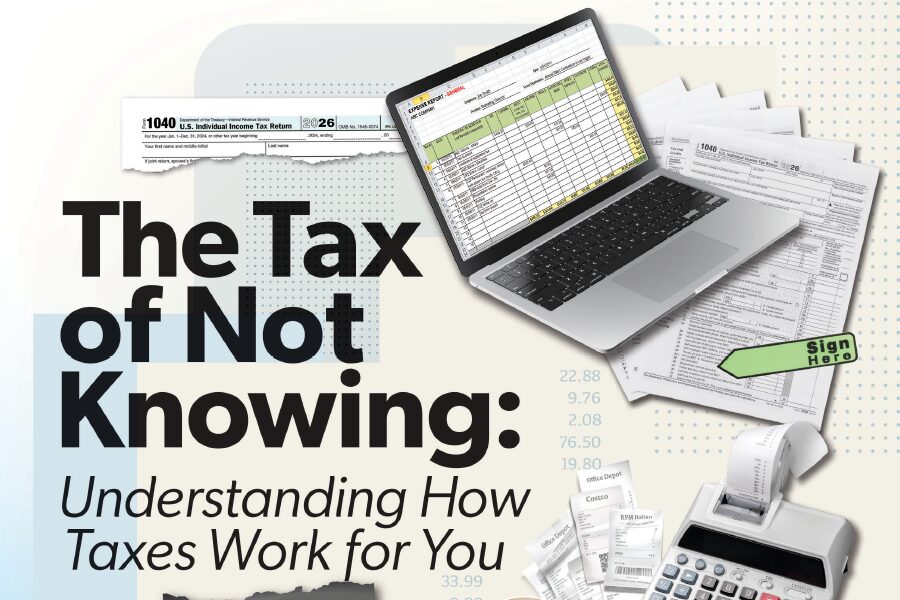

By Darion Wiggs, Wiggs CPA Tax and Accounting LLC As a Certified Public Accountant and tax strategist who works closely with real estate professionals every day, my goal is simple: […]

When artist Marisa Morán Jahn and architect Rafi Segal began designing an installation for the National Public Housing Museum, they did not keep the work confined to a studio. They […]

By Dave Naso, Chicago Association of REALTORS® When a listing goes live in a low-inventory market with strong buyer demand, the clock starts ticking: a buyer texts their REALTOR® within […]

It’s 8:45 AM, and the day is already moving fast. A seller is waiting for their listing to go live, and the property description still needs polish. A buyer has […]

One of the highlights of our 2026 Market Outlook event was hearing from Phil Clement and the team at World Business Chicago. His presentation brought something that can sometimes get […]

Leadership in real estate is measured by impact. Every day, REALTORS® help guide decisions and build relationships that shape neighborhoods, influence opportunity and strengthen communities. This work gives us a […]